How to Model Residual Errors to Correct Time Series Forecasts with Python

Last Updated on April 24, 2020

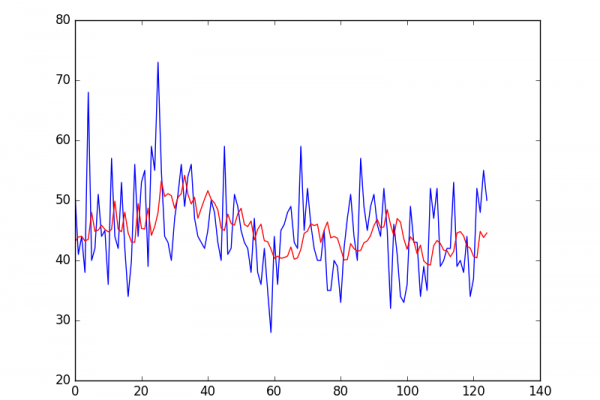

The residual errors from forecasts on a time series provide another source of information that we can model.

Residual errors themselves form a time series that can have temporal structure. A simple autoregression model of this structure can be used to predict the forecast error, which in turn can be used to correct forecasts. This type of model is called a moving average model, the same name but very different from moving average smoothing.

In this tutorial, you will discover how to model a residual error time series and use it to correct predictions with Python.

After completing this tutorial, you will know:

- About how to model residual error time series using an autoregressive model.

- How to develop and evaluate a model of residual error time series.

- How to use a model of residual error to correct predictions and improve forecast skill.

Kick-start your project with my new book Time Series Forecasting With Python, including step-by-step tutorials and the Python source code files for all examples.

Let’s get started.

- Updated Jan/2017: Improved some of the code examples to be more complete.

- Updated Apr/2019: Updated the link to dataset.

- Updated Aug/2019: Updated

To finish reading, please visit source site